Five Factors That Impact Your Credit Score

- Titan Lending

- Aug 31, 2022

- 2 min read

Minor changes to your credit structure can affect your ability to qualify for a mortgage. Everyone’s credit history will be different, but implementing good financial habits, becoming aware of your credit health, and remembering the five factors below will guide you toward building or improving your credit score.

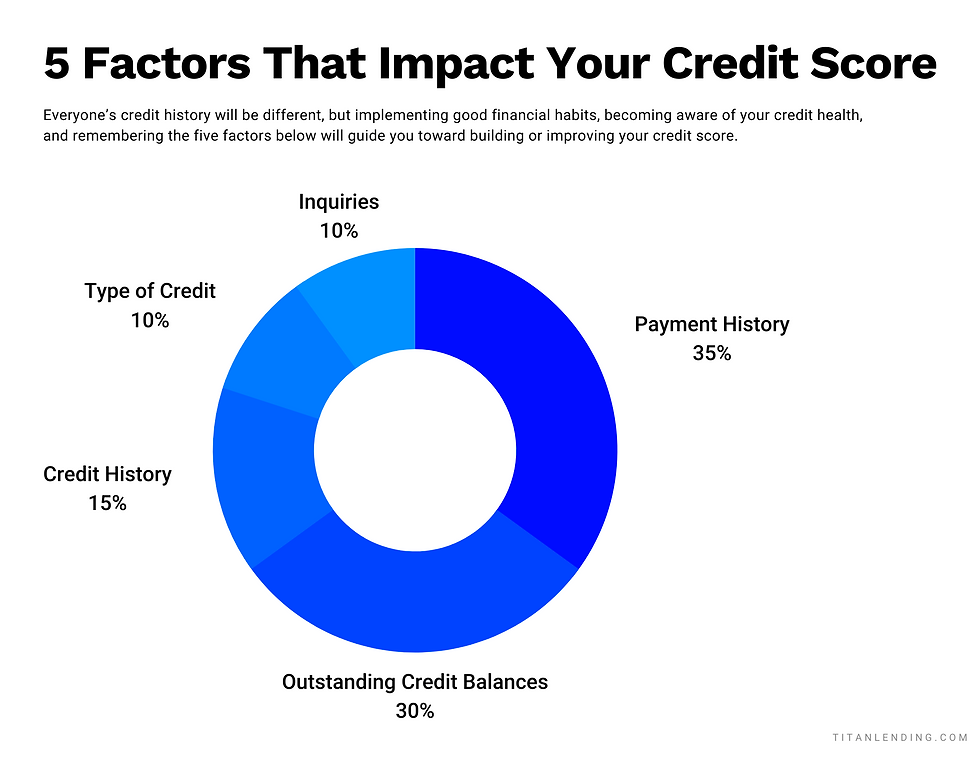

What are the factors that impact your credit score?

1. Payment History 35% Impact

Paying debt on time and in total has the most significant positive impact on your credit score. Late payments, judgments, and charge-offs all have a negative effect. Missing a high payment will have a more severe impact than missing a low payment, and delinquencies that have occurred in the last two years carry more weight than older items.

2. Outstanding Credit Balances 30% Impact

This factor marks the ratio between the outstanding balance and available credit. Ideally, it would help if you made an effort to keep balances as close to zero as possible and only use up to 30% of the available credit limit when purchasing a home.

3. Credit History 15% Impact

This credit score portion indicates the time since a credit line was established. An early borrower will always have an advantage in this area.

4. Type of Credit 10% Impact

A mix of auto loans, credit cards, and mortgages is more favorable than a concentration of debt from credit cards only.

5. Inquiries 10% Impact

This percentage of the credit score quantifies the number of inquiries made on a consumer credit within six months. Each hard inquiry can cost two to 25 points on a credit score (except for mortgage credit pulls). If you have 11 or more inquiries within six months, your first ten will reduce your credit score, but after ten, each inquiry will have no further impact on your credit score.

(NOTE: running a credit report on yourself does not affect your score.)

Your credit score can be an important factor when considering a mortgage. Ready to find out which type of loan will best suit your needs? Contact us today!

Comments